Stochastic Coherence

Deriving the laws of probability through superforecasting

In Dawid’s “Well-Calibrated Bayesian,” he nonchalantly throws around the word “coherent” without definition.

“a coherent Bayesian expects to be well calibrated.”

“...probability forecasting fits neatly into the general Bayesian world-view as conceived by de Finetti (1975). The coherent subjectivist Bayesian can be shown to have a joint probability distribution over all conceivably observable quantities.”

“the coherent sequential forecaster believes that he will be empirically well calibrated.”

What does coherent mean in these quotations? It turns out there are many definitions that are not precisely equivalent. One, in particular, is tied to forecasting and provides an argument for why any forecaster should be a subjective Bayesian. Let me present that argument, and you can tell me if you buy it.

To begin, we have to talk about logical probability again. One of the main interpretations of probability is a numerical quantification of belief. The ideal rational thinker is supposed to be able to assign a number to any metalinguistic statement, with 0 meaning they believe it’s false and 1 meaning they believe it’s true. Let’s call these numbers credences. A numerical system of credences is coherent0 if it assigns a credence of 1 to logical tautologies and if, for mutually exclusive statements A and B, the credence of “A or B” is equal to the credence of A plus the credence of B. In other words, a set of credences is coherent0 if it obeys the axioms of probability.

Bruno de Finetti thought there should be a way to derive these axioms of probability as an inevitable consequence of being rational. De Finetti initially proposed a different property of credences: credences were the values of bets a person would be willing to take about the truths of logical statements. A set of credences was coherent1 if there was no series of bets where a person was guaranteed to lose money when wagering on their beliefs no matter what the truth value of the propositions was. That is, a system was coherent1 if it was impossible to create a set of bets that a person thought had positive expected value but would always lose no matter what.1 Via a relatively simple argument, you can show that any system that is coherent1 also obeys the axioms of probability. If you are willing to bet against logical tautologies or for negative probabilities, you lose money. A coherent1 system is coherent0.

Despite its origins at the dice table, I’ve always found the motivation of probability through gambling distasteful. Especially once probability and rationality became inextricably linked after World War II. This mindset assumes that people reason only to wager and that gambling is somehow the purpose of life. The terminus of this mindset leads to a world of ubiquitous boom-and-bust gambling meme scams. It's a world where everybody thinks their cleverness will get them to outwager the other guy, never admitting that almost everyone loses while an oligarchical house wins and wins. Looking out my window in the East Bay, let me tell you that that world sucks.

Lucky for me, it turns out that coherence can be motivated in lots of different ways, and a particularly appropriate one for this blog is in terms of prediction.

Instead of our degenerate rational gambler, let’s envision a hypothetical rational forecaster who wants to assign numerical values to their beliefs of outcomes. They will be evaluated in terms of the accuracy of their predictions. The evaluation will let them express their confidence by providing numbers between 0 and 1. One such potential evaluation is through the Brier Score.

A set of credences is coherent2 if there is no set of events where there is another forecast that achieves a lower Brier score no matter the outcome of the events.

Let me give an example of an incoherent2 forecast: predicting the probability of rain tomorrow to be 70% and the probability of no rain being 40%. In this case, the Brier score if it rains is

(1-.7)^2 + (0-.4)^2 = 0.25If it doesn’t rain, the score is

(0-.7)^2 + (1-.4)^2 = 0.85However, the competing forecast of 65% for rain and 35% for no rain has Brier score

(1-.65)^2 + (0-.35)^2 = 0.245if it rains and

(0-.65)^2 + (1-.35)^2 = 0.845if it doesn’t rain. These scores are lower than the incoherent2 forecast, whether it rains or not. De Finetti says that the second forecast dominates the first forecast as it receives a better score no matter what the future brings.

I like this formulation a lot. Perhaps unsurprisingly, a coherent2 forecast obeys the axioms of probability. A coherent2 forecast must assign 1 to events that must happen. The example I gave above is of a more subtle and interesting property. Coherent2 forecasts obey the law of subadditivity: for any two mutually exclusive events A and B, a coherent2 forecast for “A or B” equals the forecast for A plus the forecast for B. Subadditivity is a bit trickier, and de Finetti proves it via a beautiful convex analysis argument. Essentially, if you have a forecast function that violates subadditivity, you can project it onto the convex hull of the indicator function of the events. This projection will have a lower Brier score no matter what values the events take. This is how I came up with the (.65,.35) forecast to dominate the (.7,.4) forecast.

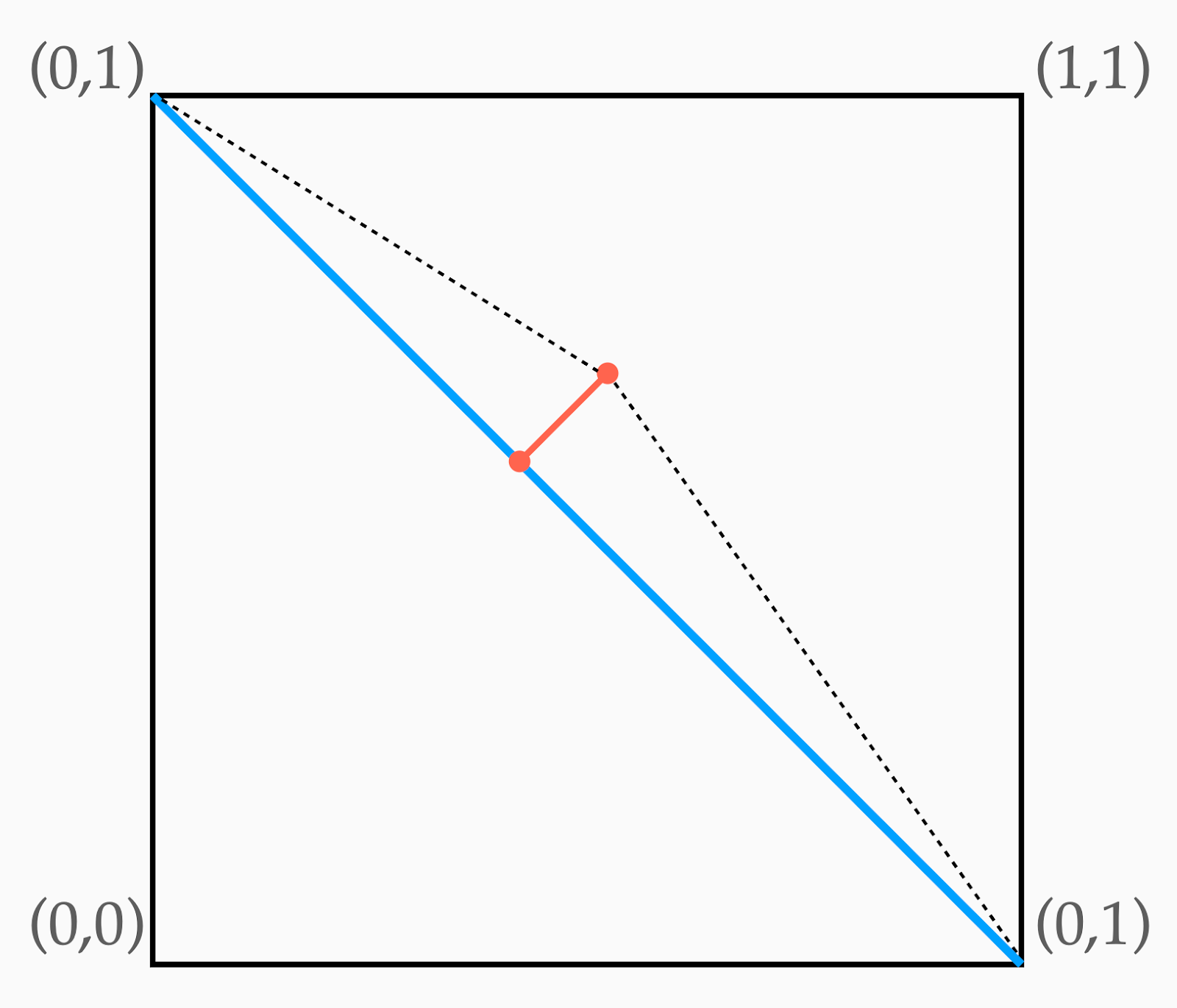

The following picture, which I recreated from some great slides of Teddy Seidenfeld, illustrates why subadditivity must hold.

For mutually exclusive, exhaustive events, there are only two potential outcomes: (0,1) and (1,0). The line in this figure draws the convex hull between (0,1) and (1,0). Any point in this convex hull will be of the form (p,1-p) for some p in between 0 and 1. If your forecast is outside the convex hull, then the projection of that forecast onto the convex hull will be closer to both (0,1) and (1,0). This means the projected forecast must have a lower Brier Score no matter what the future holds.

While De Finetti initially proposed Brier Scoring, the scoring rule itself isn’t essential. Building on the work of Lindley, Predd et al. showed that you can replace the Brier score with any continuous strictly proper scoring rule. A coherent2 forecast is never dominated by another forecast under any continuous strictly proper scoring rule. This is because the geometric argument I sketched above holds not only for the Euclidean distance but for any Bregman divergence. Math is fun.

If we pick one of the scoring rules from Monday’s post, Predd et al.’s result means that coherent2 contains coherent1. This shouldn’t be surprising, as bets are also predictions. But you don’t need to equate evaluation with potential gambling returns. What de Finetti’s argument implies is that no matter what you do, if your predictions will be strictly properly scored, you are always guaranteed a better score if you make probabilistic predictions.

Lindley takes this a step further to argue against fuzzy logic and frequentism.2 He writes, “only probabilistic descriptions of uncertainty are reasonable.”

Lindley gets over his skis. The precise statement is uncertain forecasts of logical outcomes need to be probabilistic if they are evaluated using systems that favor probabilities. Is this circular reasoning? A little!

Probabilistic descriptions are reasonable if your evaluation is a proper scoring rule. Machines scored by machines must speak in probabilities. But might we evaluate the value of forecasts and beliefs differently? Might they be assessed in nonquantifiable ways? Might they be evaluated singularly with respect to context? If so, it might be just fine to be incoherent.

Series of bets where the incoherent1 person always loses are called “Dutch Books” in philosophy. I’m pretty sure it’s connotation is racist.

In the acknowledgments, Lindley thanks Lotfi Zadeh, who invited him to present a seminar at Berkeley on the “relationship between probability and the ideas of fuzzy logic.” Zadeh challenged Lindley to find a scoring rule that would favor the laws of fuzzy logic. Lindley’s paper shows no such rule exists.

Regarding coherence in the sense of De Finetti, take a look at this footnote to my old post about probabilities, and in particular at the thesis of Peter Jones mentioned there: https://realizable.substack.com/p/probabilities-coherence-correspondence#footnote-2-141765512. The link to the paper of Mitter et al. on coherence and Kolmogorov consistency in the footnote is dead, but here is the fresh one: https://mitter.lids.mit.edu/publications/102_ondefinetti_elsev.pdf. Ultimately they say it's all about convex analysis.

The Predd et al. paper is from 2009, yet no reference there to the 2004 paper of Mitter et al., even though they are closely related.

> This mindset assumes that people reason only to wager

Can you name a better reason to reason coherently? Every decision-making-under-uncertainty problem, like it or not, is a question of how to wager.

Of course we also reason for other reasons: sometimes for fun, and sometimes (usually?) for social reasons (e.g., to show off, to convince people to do what we want, or to justify ourselves—cf. Mercier and Sperber's IMO excellent "The Enigma of Reason"). But generally the reasoning you get in those settings isn't particularly coherent, because it doesn't need to be.

> and that gambling is somehow the purpose of life...that world sucks.

Look, I hate it here too man, but I think you've got more work to do if you want to connect the historical dots from Dutch-book arguments to memecoins.

"This mindset" only assumes that one's objectives are known (i.e., non-rational or, if you like, suprarational), and that achieving those objectives may involve risk. Reasoning about what choices (wagers) to make is a means to an end, not an end in itself.

To be clear, I do think there are plenty of critiques to be made of this rationalist paradigm, both practical (e.g., what if we need to include the cost of computation in our objective?) and philosophical (e.g., people's expressed preferences are often themselves incoherent)! I just don't find the argument "gambling is gross" very compelling—the world is full of gross stuff, and ignoring it doesn't make it go away.